How to Plan and Afford Building a Custom Home in the Next 3 Years

How We Used a Custom Mortgage Calculator to Build Our Dream Home —Without Sacrificing Our Life

Thinking about building a custom home, but unsure when—or how—you can afford it? We were in the same place a few years ago.

We didn’t want to give up the life we’d worked hard to build. We didn’t want to delay our financial goals, settle for less than our dream, or feel pressure to build fast just to “get in.” What we needed was clarity. So we built our own custom mortgage calculator—a tool that helped us reverse engineer a realistic timeline, budget, and mortgage we felt good about.

Here’s how we used it, and how it helped us wait with confidence instead of rushing in.

When “What’s Your Budget?” Feels Impossible to Answer

Building a home is exciting—but also overwhelming and expensive. There’s the version you imagine, the rough numbers builders give you, and then the actual cost of creating the home you want.

When we first started dreaming, we had a strong sense of what we didn’t want to spend—but we had no idea what our ideal home would actually cost.

We weren’t ready to name a budget, and that’s one of the hardest parts in the early stages. You don’t want to pick a number just to realize later you cut out must-have features or backed yourself into a corner.

That’s why we waited. Not because we were afraid, but because we didn’t want to compromise.

We wanted to approach the process with clarity, not urgency.

Step One: We Started With the Numbers (Not the Budget)

We didn’t start with a budget—we started with a vision and a Pinterest board. Then we sent early drawings to a few builders to get rough estimates. Not exact bids, but enough to begin planning.

From there, we asked:

- What’s our dream monthly payment?

- What mortgage does that support?

- How far out are we from being able to carry that?

Most people focus on the total home price. But the monthly mortgage payment is what you feel every single day. That’s where financial peace lives—or doesn’t.

We weren’t interested in maxing out our loan. We were interested in building a life that still allowed us to take trips, eat out sometimes, and say yes to the things that mattered to us.

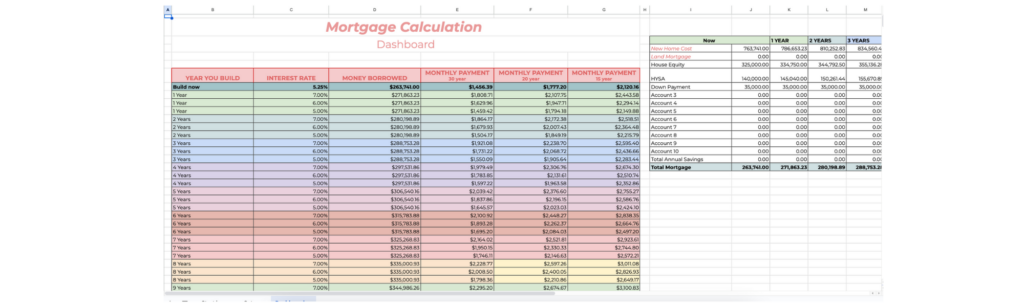

Why We Built a Custom Mortgage Calculator

We started with a simple spreadsheet—plugging in estimates, testing different down payment scenarios, and adjusting for interest rates.

It quickly turned into something more.

This wasn’t a one-size-fits-all calculator. It was built for our real life. For our actual numbers. And it grew into a tool that helped us understand:

- How our savings and equity would impact a future build

- Whether waiting six months (or twelve) would change things

- What interest rate fluctuations would mean for our payment

- How debt payoffs or side income could speed up our timeline

The more we played with it, the more confident we felt. We weren’t making guesses. We had a plan.

What’s Inside Our Mortgage Calculator

We added everything we wished other calculators included:

- Estimated home and land cost

- Your current mortgage, home equity, and debt balances

- Savings and investment totals (with optional interest growth)

- Your ideal monthly mortgage payment

- Inflation and cost increases over time (default 3%)

- Projections at multiple interest rate tiers and mortgage lengths (15, 20, 30)

- A visual timeline to show when you’re ready to build

It’s not about predicting the future perfectly. It’s about giving yourself a tool that adapts with you as life evolves.

The Real Question: What Mortgage Still Lets You Live?

One of the biggest realizations we had:

We could afford to build when we first started crunching numbers. But we wouldn’t have felt good about it.

We’d be house poor. Always watching the budget. Stressed about every purchase.

And that wasn’t our dream.

So we decided to wait—but wait with a plan. I talked about it a bit in my post about why we hadn’t broke ground yet.

Our Timeline Became Clear Once the Numbers Did

This calculator didn’t limit our dream. It helped us chase it wisely.

We went from guessing to planning.

We could look at our current situation and ask:

- How much more time would get us the mortgage we actually want?

- What happens if we save an extra $200/month?

- How does paying off our land change the equation?

- What if we sell our current home for more than expected?

Those weren’t just thought experiments. They were inputs we could plug in to see actual results. And the ripple effect of small changes was more powerful than we expected.

This tool helped us:

- Set monthly savings goals tied to our gap

- Adjust timelines based on interest rate changes

- Make informed tradeoffs instead of emotional ones

- Know exactly when it made sense to start calling builders

Suddenly, what once felt overwhelming felt doable.

It gave us a roadmap.

If You Want to Build a House in the Next 3 Years, Start Here

Here’s what I’d tell anyone in your shoes:

1. Start With the Numbers (Not Just the Pinterest Board)

Dream big—but ground that dream in real math.

2. Get a Rough Estimate Now

Even if you’re years out, early estimates give you a ballpark to plan toward.

3. Define Your Monthly Comfort Zone

Don’t just focus on the home price. Decide what monthly number allows you to still live and enjoy your life.

4. Reverse Engineer From There

Use a tool that lets you plug in your current savings, equity, and goals—and shows you when you’ll get there. If you’re interested, you can check out my tool

5. Update As You Go

Your life will shift. So should your plan. This isn’t about perfection. It’s about direction.

A Tool Won’t Build the House for You—But It Will Give You Confidence

This calculator didn’t tell us when to build. It didn’t answer every question.

But it gave us the confidence to say “not yet” without fear. It helped us focus on our values. And it made the day we finally broke ground feel not just exciting—but fully aligned.

If you’re planning to build in the next 12–36 months, here’s my advice:

Start with clarity.

Start with the numbers.

You might be closer than you think.